Indian Blue Book Survey says Second Hand Car Market 1.2 Times The Size New Car Market and is rapidly increasing

Second Hand Car Market 1.2 Times The Size New Car Market, that is a bold statement. Indian Blue Book pricing and analytics platform for new and pre-owned vehicles in India, today released the third edition of the ‘India Pre-owned Car Market Report’. The past two years have seen a coming of age of sorts for the industry, with testing of new business models, launch of new vehicle categories and rise of innovative approaches to solving problems long regarded as intractable

This is the first in-depth, definitive consumer study in the industry in about a decade of the Second Hand Car Market, where an effort is been made to understand in detail the profile of customers buying and selling pre-owned vehicles, their primary motivations and key concerns. This exclusive study was done with PremonAsia, a consumer-insight based consulting firm based out of Singapore and India.

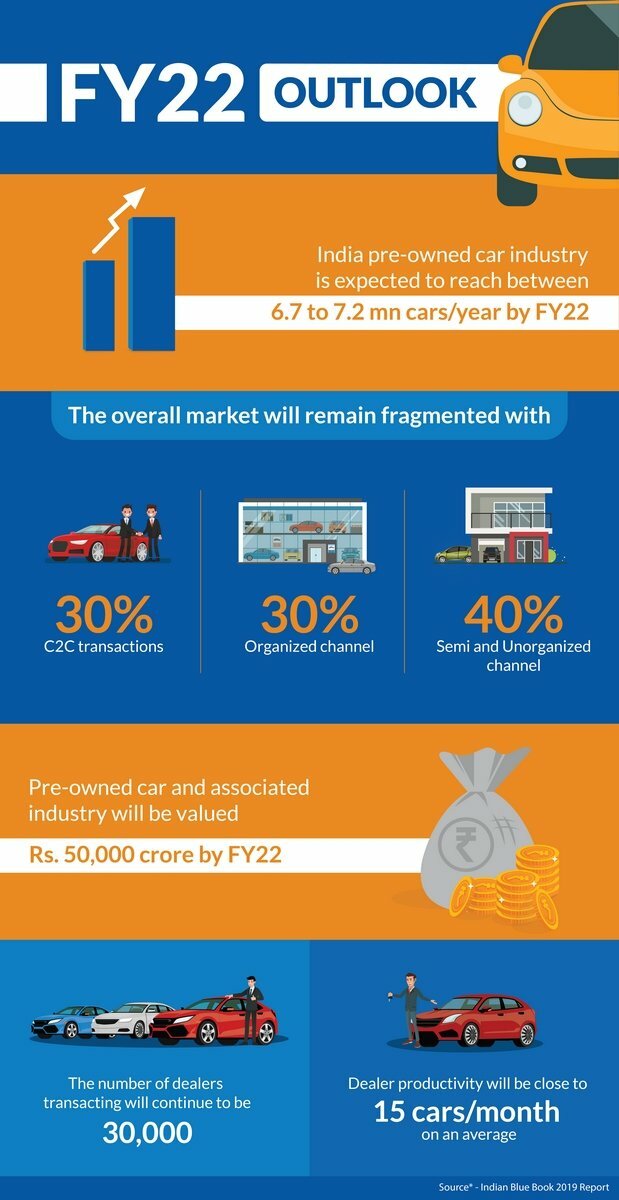

The pre-owned car market has grown steadily in FY19, it has crossed the 4 million unit mark and is 1.2x the size of new car market

The industry is seeing tail winds post the rationalization of GST to 12-18% and is seeing increased investments across the value chain from procurement to retail

If one looks at the shift in the market composition in the past decade, one would observe that the organized channel of the pre-owned car market has almost doubled its share from 10% to 18%, from FY11 to FY19

The organized market is the fastest growing channel and is reaping benefits of the changing customer preferences and belief systems

The role of digital in pre-owned car transactions has been profound, which is seen in the rapid increase in pre-owned car-related search queries that stand at over 170 million in FY19

Over the past 4 years, the investment in companies in this sector has also been to the tune of over Rs. 5,000 crores

Over 50% of cars sold in the pre-owned car market are retail worthy in FY19

The key contributor to propel this is the reduced replacement cycle of cars owing to newer launches in the mid-to-premium new car segments

Dealer footprint across India has reduced due to macroeconomic factors, especially affecting unorganized dealers. However, organized dealers continue to grow at 19% YOY

Dealer footprint across India has reduced due to macroeconomic factors, especially affecting unorganized dealers. However, organized dealers continue to grow at 19% YOY

Finance penetration in pre-owned cars is at 17% currently with a lot of headroom for growth

The average disbursement value is Rs. 3.4 lacs which is 75-80% of the LTV

Over 85% choose a pre-owned car as a stepping stone to progress towards a new car

15% consumers, classified as value seekers, continue to buy pre-owned cars, as they have a rational approach towards car ownership

The movement of two-wheeler owners to pre-owned car owners and increased composition of value seekers would fuel the growth of the pre-owned car industry

Given that pre-owned car purchase is driven by affordability and a majority of them are first time car buyers, preference towards entry-level hatchbacks and sedans is seen over 75% of pre-owned car purchases comprise hatchbacks and sedans, which are similar to the new car market

The cars bought are pre-dominantly from first owners with 72% of them being less than 5 years of age

A pre-owned car buyer tends to be steadfast, with over 40% buyers sticking to a preferred model from research to purchase. Hence, availability of the preferred model becomes the key enabler to choose the purchase channel

Similar unwavering persistence is seen in the budget-to-purchase segment with over 55% buyers tending to stick to and limit the options within the budget

However, the number of consumers who are paying for an expert evaluation has jumped 3 times from 10% to 29%, from FY09-FY19, indicating the opportunities for organized certified pre-owned market

With the demand for pre-owned cars rising, the pre-owned car ecosystem continues to grow. This has attracted multiple players to systematize the unorganized market

Internet’s growth has opened a new channel for sales initiation

Hence, even among those who did not initiate their purchase online, about 60% researched online during the purchase process

Over 54% of cars coming to the pre-owned market are retail worthy

Sellers tend to remain as car owners upgrading from a smaller segment car

Every pre-owned car is unique, which means the price of every car varies

To address the key concern of getting a fair price, a seller explores multiple avenues to ascertain the price but it continues to be dominated by discussions with friends and family

Only 10% of sellers were concerned about document and transfer process

A decade ago, over 80% of car sellers used to check with family and friends

A seller takes 18 days on an average to conclude the sale of the car, however, the expected time to closure is 10 days, which suggests the growing need for quick and convenient price

Sellers who sold their car through an organized channel got a better price in comparison to other channels

{kind=link}